ECONOMIC & FINANCIAL UPDATE

August 2006

The global economy has been performing remarkably

well in recent years. World economic growth has been

running at its strongest pace in more than three

decades, fueling a dramatic rise in commodity

prices, rapid growth in profits and better labour

market opportunities. Booming economic conditions in

China, India and a number of other emerging

economies led the way, but the industrialized

nations participated as well. For example, after

more than a decade of stagnation, Japan turned a

corner last year with its banking sector

recapitalized, deflation drawing to a close and amid

stronger domestic economic conditions. In Europe,

the corporate sector has fared well, and although

economic growth has been modest, there were signs of

improvement in late 2005 and in the first half of

2006.

In North America, economic times have also been

better than most people realize. Economic growth in

both the United States and Canada has been solid, as

unemployment fell to historically low levels and

profits advanced at a robust pace. Also, domestic

demand in the form of consumer spending and business

investment has proven strong. In Canada, the main

economic handicap has been the lagged fallout from a

high-flying Canadian dollar. Although it has been a

painful adjustment, businesses have coped well by

cutting costs and boosting their productivity in

order to limit their loss of competitiveness; as a

result, the Canadian economy expanded at a healthy

pace. Looking forward, however, it appears that

economic conditions may be less robust.

Economic expansion to moderate

In the United States, the U.S. Federal Reserve has

raised interest rates considerably from their 1.00

per cent trough in order to ensure that inflation

remains in check. The result of these higher

interest rates means that monetary policy could act

as a headwind to the economy going forward. In

addition to tempering consumer spending, and to a

lesser extent business investment, higher interest

rates are cooling U.S. real estate markets. This is

likely to dampen consumer spending as the powerful

wealth effects arising from past home price

increases, mortgage refinancing and cashing-out of

home equity wanes. As a result, TD Economics

believes that the average annual pace of U.S.

economic growth in 2007 will likely slacken.

However, a hard landing is not anticipated and some

improvement can be reasonably expected in the latter

part of the year.

Any moderation in U.S. economic growth will impact

other economies. Softer U.S. demand would likely

dampen international exports, leading to slower

economic growth in the major U.S. trading partners.

However, given the momentum in world expansion, the

overall pace of global growth is expected to remain

above its historical average, and there is little

chance that the Chinese and Indian boom could be

derailed. Canada could be adversely affected, as

exports represent roughly 40 per cent of the economy

and as 85 per cent of Canadian shipments head

Stateside. Simultaneously, the Canadian economy will

be feeling the lagged effect of the Bank of Canada’s

rate hikes delivered in late 2005 and in 2006, which

suggests some moderation in consumer spending and

housing markets. Overall, the annual pace of

Canadian economic growth is forecasted to slow

modestly in 2007, but this national perspective

masks the likelihood of continued above-average

growth in Western Canada, and a sub-par performance

in Central Canada and parts of Atlantic Canada.

Financial implications

This economic backdrop has many financial

implications.

First, weaker economic growth suggests a modest pace

of corporate profit growth in 2007. However, strong

corporate balance sheets should allow the majority

of firms to ride out any weaker economic times.

Second, commodity prices are vulnerable to a further

correction, as a slowdown in the world’s largest

economy – the United States – could result in softer

global demand for raw materials. Having said that,

price levels should remain high, supported by strong

demand from Asia. Some commodities may also break

from the general trend. So, while oil prices could

drop, natural gas prices are forecast to rise –

barring another extraordinarily mild winter.

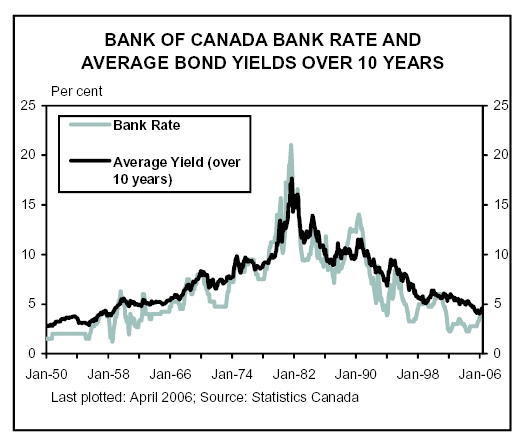

Third, interest rates are likely to decline in late

2006 and early 2007. Weaker economic growth would

lower the risks of inflation, leading to a rally in

bonds. There is also a possibility that the Federal

Reserve and the Bank of Canada could cut rates to

limit the slowdown. However, as economic conditions

gradually recover, interest rates would most likely

rise once again.

Fourth, the U.S. dollar is likely to lose ground

relative to the other major currencies, including

the Japanese yen and the euro. The Canadian dollar

could also benefit from U.S. dollar weakness, but in

recent years the dominant driver behind movements in

the exchange rate has been commodity prices.

Nevertheless, even if commodity prices decline as

anticipated, the Canadian dollar should remain

strong and it will likely hold well above its

estimated fair value of 82 U.S. cents.

Weakness will pass

Lastly, it should be stressed that the economic

slowdown should prove mild and transitory. While

economic and financial volatility may be present,

the underlying fundamentals should remain positive.

Unemployment is forecast to remain low, interest

rates are anticipated to remain modest by historical

standards, and income is likely to continue to rise.

As a result, households, businesses and investors

should not panic if there are signs of economic

moderation, as the economies should recover in the

near future. Used with permission from TD Canada Trust.

For more information please contact A. Mark Argentino

A. Mark Argentino Associate Broker, P.Eng.,

Specializing in Residential & Investment Real Estate

RE/MAX Realty Specialists Inc.

2691 Credit Valley Road, Suite 101, Mississauga, Ontario L5M 7A1

BUS 905-828-3434

FAX 905-828-2829

E-MAIL mark@mississauga4sale.com

Website: Mississauga4Sale.com