HIGHLIGHTS

HIGHLIGHTSBoth Canadian inflation and retail sales surpass expectations

Odds of a further BoC hike increase, but outcome will hinge on future data

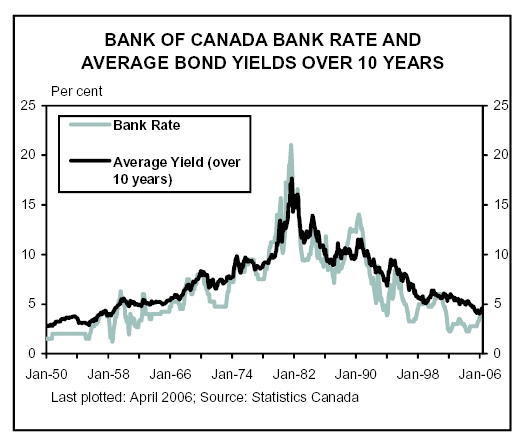

Even though the Stanley Cup will remain in the United States for another season, the spotlight on economic data swung back to Canada this week, revealing a few more pieces of the economic puzzle facing the Bank of Canada. Unfortunately, the picture has become increasingly murky as stronger-than-expected readings for both inflation and retail sales joined the spectacular May employment report released two weeks ago in stoking fears that the Bank would plow ahead with a further rate hike at their upcoming Fixed Announcement Date (FAD) on July 11th. This stands in stark contrast to the extremely dovish message conveyed in the May 24th communiqué which suggested that the tightening cycle was complete. This week presented an ideal opportunity for the Bank to express any change in this view during Governor Dodge’s speech and subsequent press conference on Wednesday. However, the Governor stuck to his guns and urged calm in the face of the recent volatility. He went on to say that the evolution of economic data since the last FAD has remained consistent with the overall outlook articulated in the latest Monetary Policy Report. Taking the Bank at their word, a case can be made to leave rates on hold once you dig into some of the details underlying the headline figures. However, the final decision will likely depend on the evolution of the data between now and the decision date.

Inflation risks far from clear

From the perspective of financial markets, the strongest piece of evidence supporting a further rate increase was the CPI report for the month of May. While energy prices continued to fuel total inflation, the real surprise was a sharp increase in the core rate of inflation, which hit a year-over-year growth rate of 2.0% – four tenths of a percentage point higher than the rate observed in April and the strongest yearly increase since December 2003. While much of this jump was due to a surge in the homeowners’ replacement costs, the effect of a regulated increase in Ontario electricity prices also played a role.

This highlights a quirk in the Bank of Canada’s definition of core inflation. Whereas traditional core simply excludes the effects of all food and energy prices, the Bank of Canada preferred measure excludes eight of the most volatile components, which removes most, but not all energy prices. The price of electricity falls into this category since it is typically regulated and, therefore, relatively devoid of monthly volatility. However, there has been a trend towards more deregulation in the electricity markets, which has translated to greater price volatility. To assess the impact, consider the traditional calculation of core inflation, which rose by 1.7% in May, matching the increase observed in the previous month. This suggests that the underlying momentum in May’s core prices may not be as strong as the Bank’s own definition would let on.

A second force exerting upward pressure on Canada’s inflation rate in May was price pressures in Alberta. This should come as little surprise, since the boom in commodity prices has propelled the Western provinces to the top of the heap of pretty much every piece of economic data, skewing the national average higher in the process. For example, core inflation in Alberta, as measured by total inflation excluding food and energy prices (Statistics Canada does not provide a provincial breakdown based on the Bank of Canada’s definition of core) was 3.6% in May, marking the eighth consecutive month that Alberta experienced the hottest inflation amongst the provinces. What is even more interesting is that all of the other provinces in Canada were below the national average. When faced with this degree of dispersion, it is important to remember that the Bank has only one policy tool at its disposal for all of Canada and will set monetary policy with the national picture in mind. While the regional variation will be a component of the analysis, policy will not react exclusively to any one province, unless it threatens to unhinge overall inflation expectations. And, this captures the Bank’s true dilemma. A red-hot Albertan economy may create upward pressures on national measures of economic activity and prices, but further modest interest rate hikes are unlikely to cool it down, while additional tightening in policy could hit other provinces quite hard.

Consumption continues to shine

The effect of higher prices was also visible in the Canadian retail sales report, which trounced market expectations as total nominal sales increased by 1.7%. However, higher gasoline prices played a significant role, accounting for over half of the total increase. When the effect of higher prices is stripped out of the calculation, retail sales increased by a more moderate 1.2%, still indicative of a strong consumer, but not as spectacular as the 1.7% headline. As noted in the “TD Consumer Pulse” released this week, the pace of consumption is expected to wane somewhat in the coming months, but will remain healthy.

So where does all of this leave the Bank of Canada? As outlined above, there certainly have been some economic indicators that have surprised on the upside in recent weeks. However, the downside is not without representation. For example, the export side of the economy is struggling with the effect of the higher dollar and things are likely to get worse before they get better as an expected mid-cycle slowdown in the United States begins to take hold over the second half of the year. Furthermore, growth in the housing market (at least in Central Canada) has shown some signs of waning in recent months. Fortunately, the Bank does have some time to decide what to do with rates and it will receive a fair bit of data between now and then. One of the most important pieces will be next Thursday’s real GDP report, which will help reveal if the mere 0.1% growth observed in April may be a sign of things to come or just an isolated touch of weakness. Another important piece of the puzzle will be the release of June’s employment report on July 7th, which will determine if the gain seen in May was just a blip or whether the labour market really does have superhuman powers. At the end of the day, while the odds of a further rate increase have materially increased in light of the recent data, it will fall to the strength of the upcoming data to conclusively tip the balance. And, regardless of whether the Bank hikes or not in July, we believe that the end of the rate tightening cycle is close at hand

Reprinted with permission from TD Canada Trust

For more information please contact A. Mark Argentino

A. Mark Argentino Associate Broker, P.Eng.,

Specializing in Residential & Investment Real Estate

RE/MAX Realty Specialists Inc.

2691 Credit Valley Road, Suite 101, Mississauga, Ontario L5M 7A1

BUS 905-828-3434

FAX 905-828-2829

E-MAIL mark@mississauga4sale.com

Website: Mississauga4Sale.com