I received an email from a reader and thought I would share the question and my answer with you.

The question from Aijaz was:

I love your site.

Thanks for keeping the data up to date.

Lots of good data on it.

Question. Do u think with interest rates going up possibly mid 2015.

This will cause a correction in pricing.

What is your opinion on the over value of canadas house pricing.

Some forecasters saying 20% drop in pricing.

Are you currently on the Buy, hold, or sell model for investment property?

My answer was:

Hello Aijaz

Thank you for your email and kind comments.

You are asking very good questions. Unfortunately, nobody can predict the future but these are my thoughts and opinion.

I can see the prime rate rising to 3.25 and maybe 3.5% by the end of next year, at the earliest. Even if/when this happens, the banks will raise their rates only slightly, I don't see them keeping in step with the Bank of Canada Rate.

Rates will only rise to keep inflation in check. I don't think that rates will cause a correction in pricing. Yes, slightly fewer people will be able to enter the real estate market due to a price increase, but I don't feel this will have a large impact on our resale market.

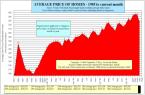

I believe that it will be some other event or combination of events that will cause our real estate market to have a correction. Our rise in prices has been unprecedented and nearly constantly upward since 1995. Logic says this cannot continue forever. Eventually the market increase in prices will slow and possibly retreat. When this will happen is anyone's guess. My opinion is that we will have a gradual slowdown of the market prices in late 2015 and into 2016, maybe only a 2 or 3% increase over that period rather compared to previous year over year increases of 4 to 10% You have to compare figures from the same period previous year as prices fluctuate during the year and you need to watch the month over month trend to get a handle on real estate prices. Year over year increases are what I am referring to.

Even if rates increase 0.5 or 1% we are still in extremely low interest rate period compared to last 50 years. I think that these low rates will be with us until at least 2020 and possibly longer. There is no reason for the rates to rise to 8% or higher and if they did, the economy would have great difficulty absorbing this shock and may crumble and correct as you and many are suggesting. I feel this is a generational phenomenon, low rates may be with us for 20 years. Rates have been exceptionally low since 2009 and I see rates staying in this very low range well into the 2020's

Our real estate market, similar to the stock market, can have a major correction in a very short period of time. Our TSX stock market has dropped (corrected - good grief I don't like that word, as it's a drop/loss/fall, not really a correction) nearly 10% since the high in mid September. In a similar way, if buyers stop paying the prices that sellers are asking and the real estate market softens then we can easily have a correction in the average price of 10% or $60,000 on the current average price of nearly $600,000 It would take about 2 to 4 months for this correction to happen.

I am always of the mindset to buy and hold for the longer term, at least 5 years and more like 10 to 20 or longer. Buy real estate, hold, reduce original amortization to 20 years, use bi-weekly accelerated payments, pay yourself by making up the $100 to $300 per month shortfall with your savings and let the tenants pay off your investment properties in 15 to 20 years. Then you can enjoy the income in your later years.

I hope this helps.

If you have more questions, please let me know.

Happy Thanksgiving to you and your family!

Mark