The Age Old Question, should you contribute to your RRSP or pay off your mortgage: Which one of these options should get your top priority?

TheStar.com - Mortgages - RRSP or mortgage: Which should get priority?

Pension actuary argues it's better to become debt-free April 30, 2007 This article is courtesy of Paul Brent

So, you can't decide whether to pay down that massive mortgage, or contribute to your meagre retirement hoard? Don't feel bad. Even investment experts are divided as to whether people should attack debt first or learn to live with debt and grow their investments through the magic of compound interest and tax-free growth.

The majority view, as espoused by the banks and the rest of the registered retirement savings plan machine, is that, rather than zero in on the mortgage, it's best to invest early and regularly in RRSP holdings. With three or four decades of tax-sheltered growth, retirement worries will take care of themselves.

"For people with normal income, and normal demands on that income, that is somewhere between bad advice and wild exaggeration," says Malcolm Hamilton, a pension actuary with Mercer Human Resource Consulting in Toronto.

A couple in their thirties who have two or three kids and a monster mortgage should not be worried about RRSP growth, he says.

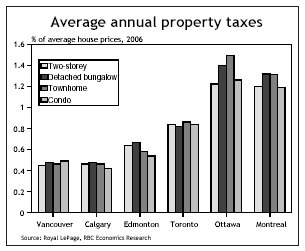

"That kind of family really has to dig out from the mortgage, and that is particularly true in Toronto and Vancouver, where the property prices are so high. There is nothing more discouraging than marching through life with no time because of your children and no money because of your mortgage and having that go on for decades."

Hamilton's advice for such couples is simple: get out of debt as quickly as possible.

"When you do the arithmetic of what kind of after-tax interest rate you are paying on your mortgage, it is a pretty high rate. The return you realize from paying it down is completely risk-free."

When you make excess mortgage payments, you attack the principal amount of the mortgage, cutting down on the interest you'll pay over the lifetime of the mortgage. Because you have wiped out all those future interest payments that would have been made with after-tax earnings, you save the interest and the tax on that interest as well.

Compare that guaranteed 6 per cent return on your extra mortgage payments to the risky potential of perhaps an 8 per cent return with an RRSP, and paying down the mortgage looks like a safe bet.

"The average Canadian couple doesn't need to maximize their RRSPs and certainly doesn't need to catch up on unused RRSP room.

"They might as well just go with the mortgage," Hamilton says.

"The key is, when the mortgage is finished, you have to do the disciplined thing, which is take the money that used to be going to the mortgage and plough it together with all your tax refunds into the RRSP and make up for lost time."

Hamilton doesn't believe in the theory that a typical couple need to replace 70 per cent of working income in their retirement. They will be mortgage-free, probably free of child-related expenses and not shelling out for work-related expenses such as clothing, lunches and transportation.

Hamilton estimates most of us can live quite comfortably on half of our pre-retirement income.

Hamilton's mortgage-first argument may be heresy to the RRSP industry, but the point generates some sympathy from Frank Wiginton, a Toronto-based financial planner.

"This whole argument about RRSPs versus mortgage fundamentally comes down entirely to the people and what their goals are," Wiginton says. "Some people value being debt-free over being financially secure. Obviously, the best thing is to try to do both."

The financial planner maintains, however, that if people had the same discipline in making RRSP contributions as with mortgage payments, they would be farther ahead financially.

"People think, `Oh, it's my RRSPs, and I'm not obligated the way I am with my mortgage,' and they let it slide."

As a compromise, Wiginton suggests that a family pay the mortgage, make RRSP contributions and apply RRSP tax refunds to the mortgage principal in lump-sum payments every year.

The financial planner also created three scenarios using the mortgage-only, RRSP-first and lump-sum approaches.

They each envisage a 35-year-old in a Toronto-area house with a $330,000 mortgage at 5.5 per cent on a five-year term with a 25-year amortization and a monthly payment of $2,000. (All figures are approximate, and spouse and children are not included in the calculation.)

This mythical household has $10,000 per year in extra cash, which could be put in RRSPs, thrown at the mortgage or both.

Putting that $10,000 against the mortgage will save $25,000 over the lifetime of the mortgage and reduce the life of the mortgage by about 1.5 years at current interest rates, according to Wiginton.

Putting the $10,000 in an RRSP that generates an average return of 8 per cent over 23.5 years (the same span as the reduced mortgage) would generate $50,000 on top of the initial investment.

Based on a typical 35 per cent tax bracket, the contribution would also generate a tax refund of $3,500.

Scenario three involves making the RRSP payment of $10,000 and putting the $3,500 tax refund against the mortgage.

That would save $9,500 in mortgage interest and reduce the amortization period by about six months.

"Everybody's situation is going to be different," Wiginton concluded.

"Go out and find a certified financial planner to help you with this, someone who can run the different scenarios for you, talk about what your personal likes and dislikes are. Is financial security more important, or is debt reduction more important?"

Read more about how you can pay your mortgage off quicker

For more information please contact A. Mark Argentino

A. Mark Argentino, Broker, P.Eng.,

Specializing in Residential & Investment Real Estate

RE/MAX Realty Specialists Inc., Brokerage

2691 Credit Valley Road, Suite 101, Mississauga, Ontario L5M 7A1

BUS. 905-828-3434

FAX. 905-828-2829

E-MAIL: mark@mississauga4sale.com

Website: Mississauga4Sale.com