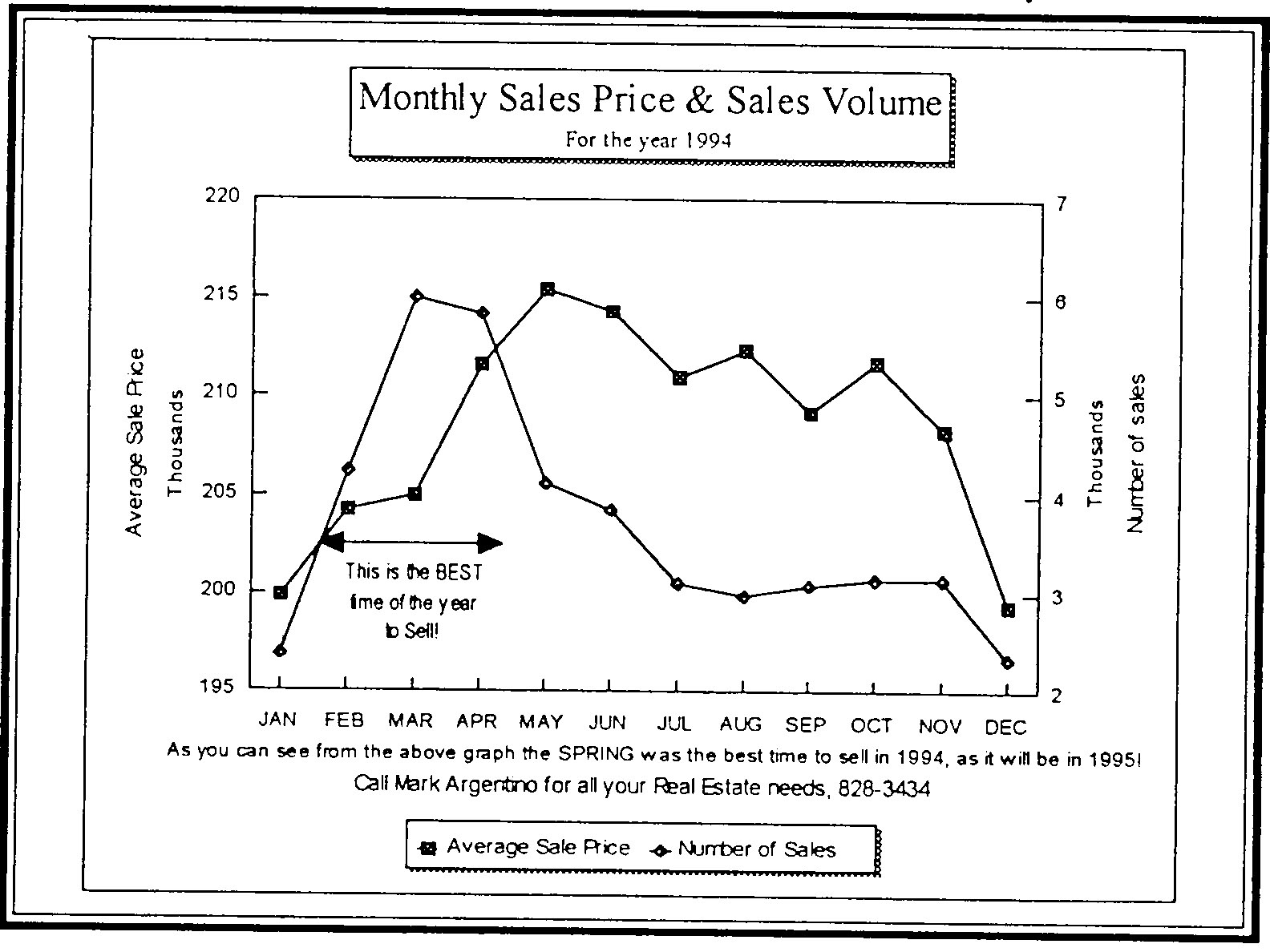

This is a 'great news' article for people taking out new mortgages or up for renewal. Mortgage rates increased significantly in October and are now falling again. Good news indeed!

Thanks

Mark

After the significant jump in fixed mortgage rates in mid-October, it was appearing as though the sub-four percent 5 year fixed mortgage rate had become history.

Here we are 6 weeks later and they are back and further decreases are expected.

There are many 5 year fixed rate programs available with the best rates being found on mortgages closing within 30 days. The lowest 'quick close' 5 year fixed rate available now is 3.84%, however I anticipate that dropping a little further within the next week.

The lowest rate on a 5 year variable is currently 2.15% (prime -0.10%), but we can expect that to drop to 2.00% (prime -0.25%) soon.

The lowest quick close mortgage rate specials often have limited prepayment options, which some people will shy away from as they may plan on prepaying more per year than the 5% maximum, even though over 90% of home owners do not take advantage of their prepayment options.

People are willing to pay significantly higher interest rates just so they can have the 'option' of prepaying their mortgage because they don't want to have to face any sort of penalty if they did choose to prepay more than the maximum.

But if mortgage seekers were to question this penalty with their mortgage professional, they would find the results quite astonishing.

Let's say for example you have a $300,000 mortgage at 3.84% with a limited prepayment option of 5%. Under the terms of their mortgage commitment, you would be allowed to prepay up to $15,000 per year.

Now, if you were to prepay the entire mortgage, your penalty would be three months interest which would be approximately $1,300 depending on what point you choose to prepay (with the extremely low rates today, the penalty will be 3 months interest and not the interest rate differential, which is what is causing the high penalties for people paying out their mortgages in today's low-rate market).

Now let's say you wanted to prepay 15% in their first year, which would be a total of $30,000 more than the maximum. The so called 'penalty' in this case would only be around $130, yet you would be canceling out thousands of dollars in interest and would save $288 on your scheduled mortgage payments in your first year alone.

This is based on today's lowest regular 5 year fixed mortgage rate of 3.99% (most banks and mortgage brokers still have regular rates around 4.19%, which would be $684 savings in the first year)

This is why it is so important for mortgage seekers to ask questions when dealing with their mortgage professional and adequately explain their plans as many mortgage professionals may not take the time to adequately explain the different options to their clients.

Ask questions and be informed and make sure you deal with someone who is going to put your needs first.

Today's lowest mortgage interest rates:

1 year 2.55%

2 year 2.95%

3 year 3.45%

4 year 3.85%

5 year 3.84% (30 day quick close)

5 year 3.99% (regular)

3 year variable 2.00% (prime -0.25%)

5 year variable 2.15% (prime -0.10%)

I hope this finds you Happy and Healthy!

All the Best!

Mark

A. Mark Argentino

P. Eng. Broker

Specializing in Residential & Investment Real Estate